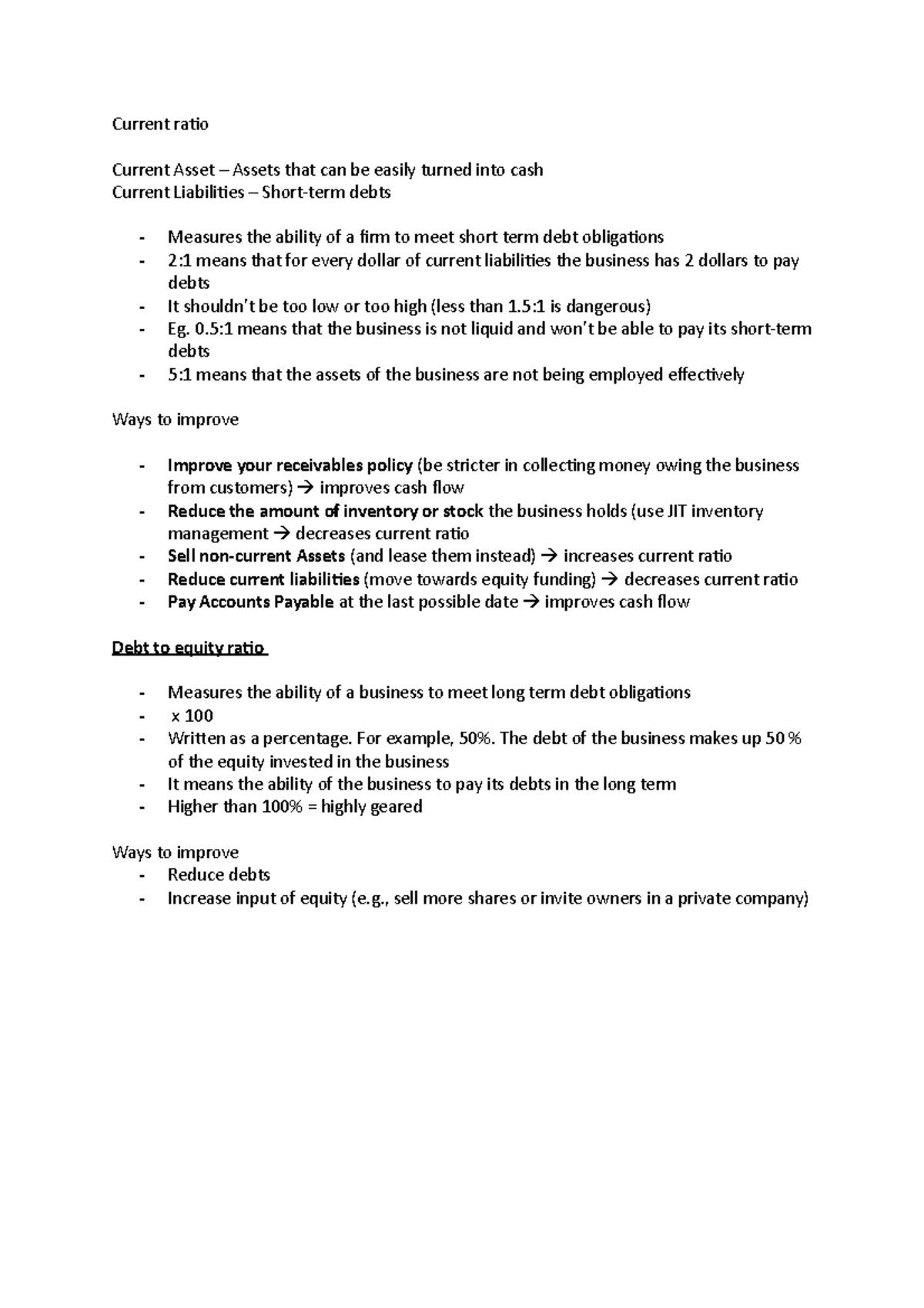

For example, if a company’s current assets are $80,000 and its current liabilities are $64,000, its current ratio is 125%. The current ratio expressed as a percentage is arrived at by showing the current assets of a company as a percentage of its current liabilities. The current ratio relates the current assets of the business to its current liabilities. Finally, the operating cash flow ratio compares a company’s active cash flow from operating activities (CFO) to its current liabilities. This allows a company to better gauge funding capabilities by omitting implications created by accounting entries.

Liquidity comparison of two or more companies with same current ratio

A company with a current ratio of less than 1 has insufficient capital to meet its short-term debts because it has a larger proportion of liabilities relative to the value of its current assets. Business owners and the financial team within a company may use the current ratio to get an idea of their business’s financial well-being. Accountants also often use this ratio since accounting deals closely with reporting assets and liabilities on financial statements. Tracking the current ratio can be viewed as “worst-case” scenario planning (i.e. liquidation scenario) — albeit, the company’s business model may just require fewer current assets and comparatively more current liabilities. If a company has to sell of fixed assets to pay for its current liabilities, this usually means the company isn’t making enough from operations to support activities. Sometimes this is the result of poor collections of accounts receivable.

What is your risk tolerance?

Clearly, the company’s operations are becoming more efficient, as implied by the increasing cash balance and marketable securities (i.e. highly liquid, short-term investments), accounts receivable, and inventory. In comparison to the current ratio, the quick ratio is considered a more strict variation due to filtering out current assets that are not actually liquid — i.e. cannot be sold for cash immediately. A Current Ratio greater than 1 indicates that a company has more assets than liabilities in the short term, which is generally considered a healthy financial position.

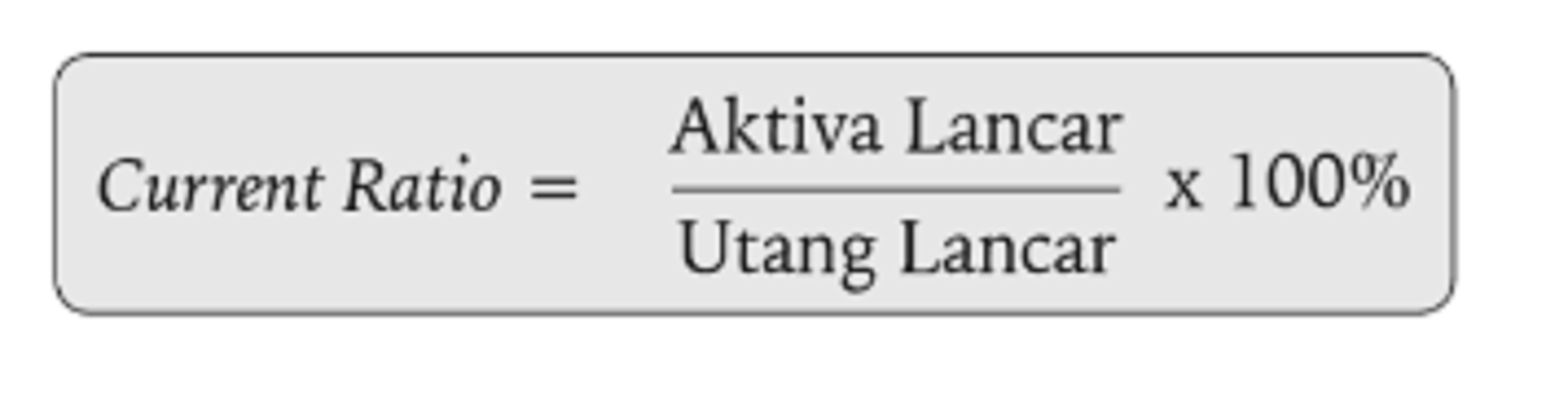

- In other words, it is defined as the total current assets divided by the total current liabilities.

- For example, if a company has $100,000 in current assets and $150,000 in current liabilities, then its current ratio is 0.6.

- It measures how much creditors have provided in financing a company compared to shareholders and is used by investors as a measure of stability.

- During times of economic growth, investors prefer lean companies with low current ratios and ask for dividends from companies with high current ratios.

- This ratio works by comparing a company’s current assets (assets that are easily converted to cash) to current liabilities (money owed to lenders and clients).

- Furthermore, the study found that the correlation between profitability and liquidity ratios is stronger for firms with higher leverage.

Formula in the ReadyRatios Analysis Software

But a too-high current ratio may indicate that a company is not investing effectively, leaving too much unused cash on its balance sheet. In other words, it is defined as the total current assets divided by the total current liabilities. If a company’s current ratio is less than one, it may have more bills to pay than easily accessible resources to pay those bills.

Since this inventory, which could be highly illiquid, counts just as much toward a company’s assets as its cash, the current ratio for a company with significant inventory can be misleading. Because inventory levels vary widely across industries, in theory, this ratio should give us a better reading of a company’s liquidity than the current ratio. Current assets (also called short-term assets) are cash or any other asset that will be converted to cash within one year.

Get in Touch With a Financial Advisor

To calculate the current ratio, divide the company’s current assets by its current liabilities. Current assets are those that can be converted into cash within one year, while current liabilities are obligations expected to be paid within one year. Examples of current assets include cash, inventory, and accounts receivable. Examples of current liabilities include accounts payable, wages payable, and the current portion of any scheduled interest or principal payments.

Therefore, it is critical for such companies to maintain a good liquidity position in order to ensure their profitability. The current ratio helps investors and creditors understand the liquidity of tax preparer mistakes a company and how easily that company will be able to pay off its current liabilities. So a current ratio of 4 would mean that the company has 4 times more current assets than current liabilities.

Other similar liquidity ratios can supplement a current ratio analysis. In each case, the differences in these measures can help an investor understand the current status of the company’s assets and liabilities from different angles, as well as how those accounts are changing over time. This is why it is helpful to compare a company’s current ratio to those of similarly-sized businesses within the same industry. The current ratio is called current because, unlike some other liquidity ratios, it incorporates all current assets and current liabilities.

Current ratio is equal to total current assets divided by total current liabilities. A high current ratio is generally considered a favorable sign for the company. Creditors are more willing to extend credit to those who can show that they have the resources to pay obligations. However, a current ratio that is too high might indicate that the company is missing out on more rewarding opportunities. Instead of keeping current assets (which are idle assets), the company could have invested in more productive assets such as long-term investments and plant assets. The current ratio is a liquidity and efficiency ratio that measures a firm’s ability to pay off its short-term liabilities with its current assets.

Large retailers can also minimize their inventory volume through an efficient supply chain, which makes their current assets shrink against current liabilities, resulting in a lower current ratio. The current ratio measures a company’s capacity to meet its current obligations, typically due in one year. This metric evaluates a company’s overall financial health by dividing its current assets by current liabilities. In other words, «the quick ratio excludes inventory in its calculation, unlike the current ratio,» says Johnson.

Comments by Леонид Романов