Shareholders’ equity refers to the owners’ (shareholders) investments in the business and earnings. A business can now use this equation to analyse transactions in more detail. The concept of the expanded accounting equation does not extend to the asset and liability sides of the accounting equation, since those elements are not directly altered by changes in the income statement. Thus, there is no need to show additional detail for the asset or liability sides of the accounting equation.

Will AI Replace My Job? Future-Proof Your Career & Income

Notes receivable is similar to accounts receivable in that it ismoney owed to the company by a customer or other entity. Thedifference here is that a note typically includes interest andspecific contract terms, and the amount may be due in more than oneaccounting period. Insurance, for example, is usuallypurchased for more than one month at a time (six months typically).The company does not use all six months of the insurance at once,it uses it one month at a time. As each month passes, the company will adjustits records to reflect the cost of one month of insuranceusage.

- Recall that the basic components of even the simplest accounting system are accounts and a general ledger.

- Some commonexamples of assets are cash, accounts receivable, inventory,supplies, prepaid expenses, notes receivable, equipment, buildings,machinery, and land.

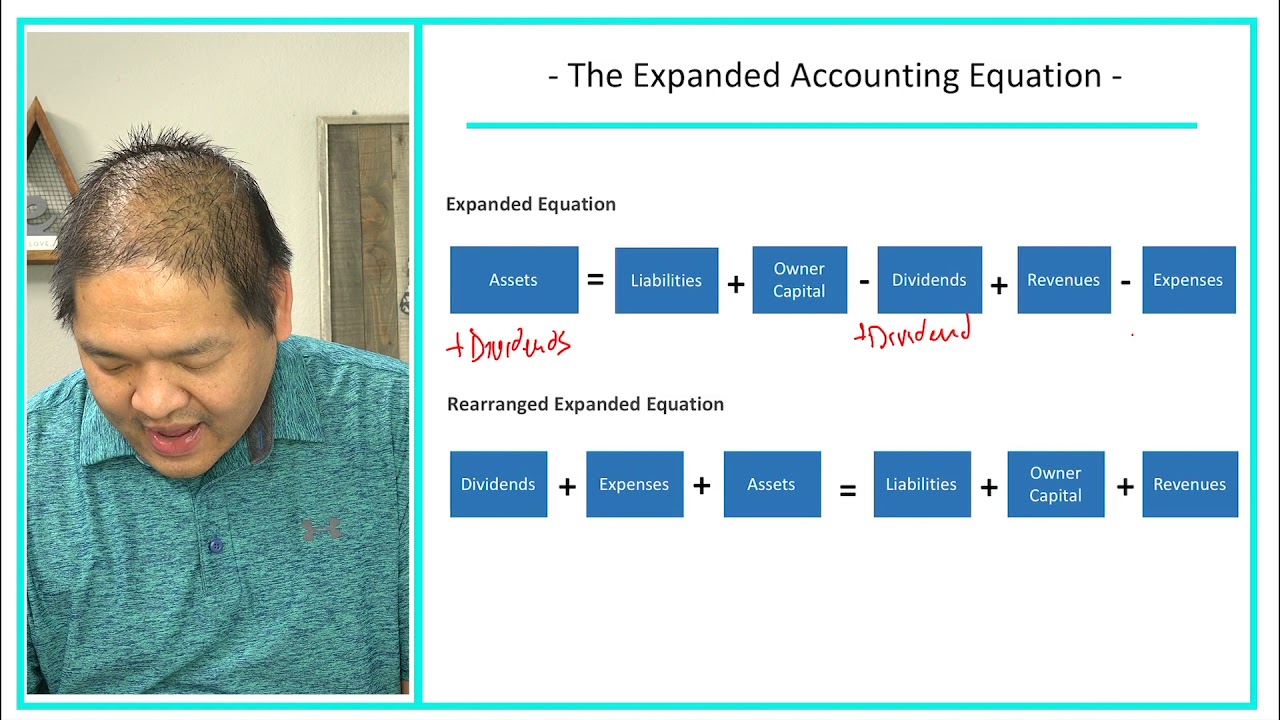

- Stockholder’s equity refers to the owner’s(stockholders) investments in the business and earnings.

- See the article “Thecontentious debit—seriously” on continuous debt for furtherdiscussion of this practice.

- As you can see with this example, the basic accounting equation remains balanced although we’ve split the stockholders’ equity into its components.

The Expanded Accounting Equation for a Sole Proprietorship

These twocomponents are contributed capital and retained earnings. A notes payable is similar to accounts payable in that thecompany owes money and has not yet paid. Some key differences arethat the contract terms are usually longer than one accountingperiod, interest is included, and there is typically a moreformalized contract that dictates the terms of the transaction. Recall that the basic components of even the simplest accountingsystem are accounts and a general ledger. Accounts shows all thechanges made to assets, liabilities, and equity—the three maincategories in the accounting equation.

How the Expanded Accounting Equation Works

Revenues and expenses are often reported on the balance sheet as «net income.» Revenue refers to the amount of money the company generated in operating its business. Contributed capital, also known as the paid-in capital, refers to the capital provided by the shareholder to the company. Applying this example to your situation and numbers can give you a comprehensive overview of your business’s financial state over time. You contributed $50,000 from personal resources into the business’s bank account and took a $30,000 loan from the bank. This dual-impact mechanism ensures the balancing nature of the equation.

Unearned revenue represents a customer’sadvanced payment for a product or service that has yet to beprovided by the company. Since the company has not yet provided theproduct or service, it cannot recognize the customer’s payment asrevenue, according to the revenue recognition principle. The company owing the productor service creates the liability to the customer. The expanded accounting equation, on the other hand, presents an in-depth analysis of a company’s finances.

Examples

Even though the business does not have to pay the bill until June, the business owed money for the usage that occurred in May. Therefore, the business must record the usage of electricity, as well as the liability to pay the utility bill, in May. Organizations use the equation to understand a holistic and descriptive financial statement picture. It can be used for deep diving into the organization’s financial transactions, thereby also in the detailed analysis of the financial statements. Therefore, always consult with accounting and tax professionals for assistance with your specific circumstances.

Cash includes paper currency as well as coins, checks, bank accounts, and money orders. Cash activities are a large part of any business, and the flow of cash in and out of the company is reported on the statement of cash flows. The owners’ investments in the business typically come in the form of issued shares and are called contributed capital. Owners/shareholders turbotax live 2021 can invest by contributing cash or some other asset. Essentially, anything a business owes and has yet to pay within a period is considered a liability, such as salaries, utilities, and taxes. Equipment examples include desks, chairs, and computers; anything that has a long-term value to the business that is used in the office.

Since corporations, partnerships, and sole proprietorships are different types of entities, they have different types of owners. For instance, corporations have stockholders and paid-in capital accounts; where as, partnerships have owner’s contribution and distribution accounts. Thus, all of these entities have a slightly different expanded equation. As you generate more complex transactions with multiple impacts on various facets of equity, you’ll find that repeatedly employing an expanded accounting equation can offer a comprehensive diagnosis of financial health. The expanded accounting equation is an elaborated version of the basic accounting equation, which allows you to get a more detailed look at the financial position of your business. Accounts payable recognizes that the company owes money and has not paid.

The equation provides an application when executing simple transactions, including injecting capital into the business or purchasing assets with cash. As you dive deeper into understanding this equation, you will see a clear picture depicting how business operations affect company finances down to expenses and revenue levels. Let’s illustrate the expanded accounting equation with an example. Diving deeper into your equity section by including revenues, expenses, and owner withdrawals makes you more conversant with your business dynamics. Let the expanded accounting equation be your guide in fraught moments like these.

Stated more technically, retained earnings are a company’s cumulative earnings since the creation of the company minus any dividends that it has declared or paid since its creation. One tricky point to remember is that retained earnings are not classified as assets. Instead, they are a component of the stockholder’s equity account, placing it on the right side of the accounting equation. Another component of stockholder’s equity is company earnings.These retained earnings are what the company holds onto at the endof a period to reinvest in the business, after any distributions toownership occur.

Beginning retained earnings refers to the earnings that have been kept by the company at the beginning of the accounting period compared to the previous period. Now, let’s say your company generates revenue of $20,000 and incurs expenses worth $5,000 during its first operating period with no withdrawals made by the owner. For example, a company uses $400 worth of utilities in May but is not billed for the usage, or asked to pay for the usage, until June. Even though the company does not have to pay the bill until June, the company owed money for the usage that occurred in May. Therefore, the company must record the usage of electricity, as well as the liability to pay the utility bill, in May. For example, a business uses $400 worth of utilities in May but is not billed for the usage, or asked to pay for the usage, until June.

Comments by Леонид Романов